VAT in Europe

What You Must Know About VAT in Europe, if You Have Customers in Europe

If you’re a business anywhere in the world, and you have customers in the European Union, listen up!

It is time to get severe about VAT in Europe. For those who don’t understand, VAT is Value-Added Tax: the tax you ought to be applying to almost every single sale you make in the EU, along with the tax you ought to be paying back into the EU each quarter.

For decades, many businesses selling goods and services in the EU have thought that if they paid taxes in their home country, they were as good as gold. But that’s not the case anymore.

Our sales outsourcing consultancy a supplier of digital products to EU customers, you’re responsible for charging, collecting, reporting, and submitting VAT in Europe to individual governments. Yes, this means across all 28 EU member states at their various VAT rates.

But never fear! We’ve made VAT simple for you: we’ve gathered all of the essential information, answered all the questions floating around in your head, and laid out everything about VAT for non-EU businesses in one place.

Let’s get started.

What is VAT in Europe?

We can answer the most obvious question first. VAT is Value-Added Tax, a consumption tax that applies to all goods and services, physical or digital. Every time a customer purchases a good or service in the EU, they pay VAT on the spot.

The vendor (your business) gathers the VAT from the customer and pays some or all of it to the government. In this way, you can consider yourself to be a sort of tax broker. It’s not your cash paying for the VAT; you’re only gathering and submitting the customer’s money to the government.

That’s why it’s essential to know when to charge VAT in Europe to your EU customers: if you don’t bill the customer for VAT in Europe, you will be paying it out of pocket.

The government will still expect the taxes from you, whether you knew to add VAT or not.

Why are non-EU businesses responsible for VAT in Europe?

Since European governments need to guarantee they receive taxes on all products and enterprises consumed by their residents — even merchandise and services originating from other parts of the world. Physical items are taxed at customs. Digital items don’t cross any borders to go through customs; so, digital items have VAT added.

If foreign businesses weren’t required to charge VAT, imagine the disadvantage that would place on EU-based businesses: their products would cost more. Their local customers would look outside the country to find something cheaper, and EU businesses would suffer. Then, when the EU businesses suffer and make fewer sales, their governments collect less tax.

So, requiring non-EU businesses to charge VAT in Europe evens the playing field for native vendors, and it increases the EU governments’ tax revenues.

How should a non-EU business handle VAT in Europe?

Register your company for VAT in Europe.

Verify your customer:

Who are they? Where are they?

Charge VAT, if you need to.

Provide detailed VAT invoices. (And keep records of them, too!)

Submit quarterly VAT returns.

We’ll break it all down for you.

Step 1: How does a non-EU business register for EU VAT (VAT in Europe)?

If you sell digital products: You can register for VAT in the EU member state of your choice. That gives you 28 countries to choose from! If you need an English-speaking base, the obvious option is Ireland.

Once you’ve chosen where you want to base your EU tax operations, register for a VAT Mini One-Stop Shop (MOSS) with that local tax authority; you can do this online. Find the “non-Union scheme” option, as this process is designed for non-EU businesses.

A MOSS allows you to consolidate all of your EU VAT into one single tax return, even if your customers live in multiple different countries. The MOSS option, however, is an option only when you sell digital products.

Let’s say you choose to register in Ireland. You apply for a VAT MOSS on the Irish Tax and Customs website. You sell to customers in France, Germany, The Netherlands, and Italy. When tax season comes around, you submit one VAT return to your MOSS in Ireland. Your Irish MOSS then calculates how much VAT should be returned to the tax authorities in France, Germany, The Netherlands, and Italy — and distributes all of that for you.

A quick recap of how to register for EU VAT:

Choose an EU country.

Go to their MOSS website.

Look for the “non-Union scheme”.

Register

Receive your VAT number!

If you sell Physical Products, then you need to VAT register in the country where you will store those products.

That means that if you store your physical products in your country, and you ship them to the destination country, you do not need to VAT register in the country that you ship your goods to (unless you exceed the threshold limit see more information below).

This, however, means that you will have higher shipping costs and extended periods to deliver your goods, and if you are outside of the European Union, customs will apply.

All those factors will make your product less competitive; that’s why you should consider storing your goods in the European country that you want to sell to.

If you are from overseas, storing in one European country and selling and shipping from there to the others is something that will make your business much more competitive than it is now.

A German customer, for example, will be way less reluctant to order your item from the UK because he knows he will not have to pay customs and because he knows he will get his item delivered within some days and not weeks.

How can you do that? By having a fiscal representative on the country of your choice.

Is it challenging for you to do that? The answer might surprise you. Click here and book a free consultation with us.

Step 2: What should you verify about your customers in the EU?

You must check two things about your EU customers: who they are and where they are. The first decides whether you charge them VAT in Europe, and the second determines how much.

Figure out who they are:

When you make a deal in the EU, ask for the purchaser’s VAT in Europe number.

Businesses will have one; private individuals won’t. Sadly, a few purchasers may endeavour to pretend that they are businesses to evade the tax; so, they’ll present a fake VRN. For that reason, check to ensure each VRN is legitimate. You can utilize this simple VIES approval device from the European Commission.

Determine where they are:

Notwithstanding asking for the purchaser’s VAT number, you additionally need to ask for confirmation of their area. Their area will decide the rate of VAT you add to the deal because each EU member state has its own particular rate.

Next, to demonstrate to the government that you’re charging enough VAT, you need to demonstrate where your customer lives. Along these lines, when making a deal, generously ask for two of the following bits of information:

– Billing address

– Location of the customer’s bank

– Country that issued the credit card

– The IP address location of the buyer’s device

– Country of the SIM card (in cases where the purchase was made on a mobile device)

Finally, document this location evidence and keep it on record for ten years.

Step 3: When does a non-EU business have to charge VAT in Europe?

Not always. It depends on where your customer is and whether your customer has a valid VAT registered number, or VRN.

If they don’t have a VRN, charge VAT; this implies your customer is an ordinary end-purchaser. It’s your usual B2C exchange. You should charge VAT on the deal, and then follow the rest of the protocol we explained above.

If they do have a valid VRN, do not charge VAT; this means your customer is a fellow business, and, therefore, you’re exempt from charging VAT; you don’t have to worry about it. The transaction is covered by the reverse-charge mechanism, which also makes your life easier as a seller if you are selling B2B. With the reverse charge mechanism, the buyer is responsible for filing VAT on the transaction. Since European companies can be reimbursed for any VAT they spend on products to help run the business, it’s more efficient if they simply keep the money in the first place — rather than pay it to you and later reclaim it from the government.

Step 4: What is a proper VAT invoice? What are the best practices for VAT in Europe invoicing?

A VAT invoice includes quite a bit more information than an average invoice. Each invoice should contain:

Your business’s name and address

Your business’s VAT number

Invoice date

Invoice sequencing number

Buyer’s name and address

Buyer’s VAT number. If you are using the reverse charge mechanism, you must also add the following text: “EU VAT reverse charged”.

VAT (amount and rate) applied to each item

Final amount after VAT is added

The currency used

Step 5: What’s the deal with submitting VAT in Europe returns?

For digital products: Submit one EU VAT return to your MOSS at the end of each quarter. Every three months, four times a year — you get the idea. From the last day of each quarter, you have 20 days to file and pay. So, the deadlines are as follows:

– 20 April — for the first quarter, ending 31 March

– 20 July — for the second quarter, ending 30 June

– 20 October — for the third quarter, ending 30 September

– 20 January — for the fourth quarter, ending 31 December

Submit your return online. You’ll need your records of VAT invoices to complete the filing.

Something to keep in mind: if you made any sales in a different currency (i.e. in the Danish Krone, but your MOSS uses the Euro), you will need to convert those amounts to the official currency of your MOSS. Use the European Central Bank’s official exchange rates.

Based on the information you enter; the MOSS website will automatically calculate how much VAT you owe. Then you’ll receive instructions on how to complete the payment.

Are non-EU businesses eligible for VAT in Europe refunds?

Yes; if you overpay VAT through the VAT MOSS scheme, you’ll get the money back. But it won’t be from your MOSS; the refund will come directly from the various tax authorities where your customers live. So, you’d get a partial refund from France, from Germany, from The Netherlands, or Italy.

The great thing is that refunds are deposited directly to your bank account, according to the bank information you provided in your MOSS registration. So, make sure those details are up-to-date!

Can a non-EU business just ignore VAT in Europe?

Legally, no. If you choose to not comply with EU VAT law, you risk getting caught by tax authorities. With that comes paying for years of back taxes, plus penalties for not following the rules. A blow like that could potentially ruin a small business. Moreover, if it turns out that you’ve intentionally broken the law, you could find yourself in court. No one wants to be convicted of fraud, right?

If you sell Physical Products, once you do your VAT fillings, all the VAT that you paid in the country (for example, the VAT for importing the goods in one country) will be deducted from the VAT you collected from your clients. In each country that you are VAT registered, you will do the same procedure either quarterly or monthly (depending on the country where you are VAT registered).

If you are selling Physical Products in the EU, the complexity of paying VAT is greater than when you sell Digital Products; however, if you compare the benefits you will have, its worth it.

Imagine if you could sell your products directly in the European Union country of your choice? In Germany, for example, or in France: huge markets with huge potential to generate a respectable income for you. Think of how much less competition you will have in Europe and how much you could save if you could avoid Distributors and the channel — if you could sell your products directly to your potential clients. It is not as difficult as you think. A sales outsourcing company can help.

Click here and book a free consultation with us.

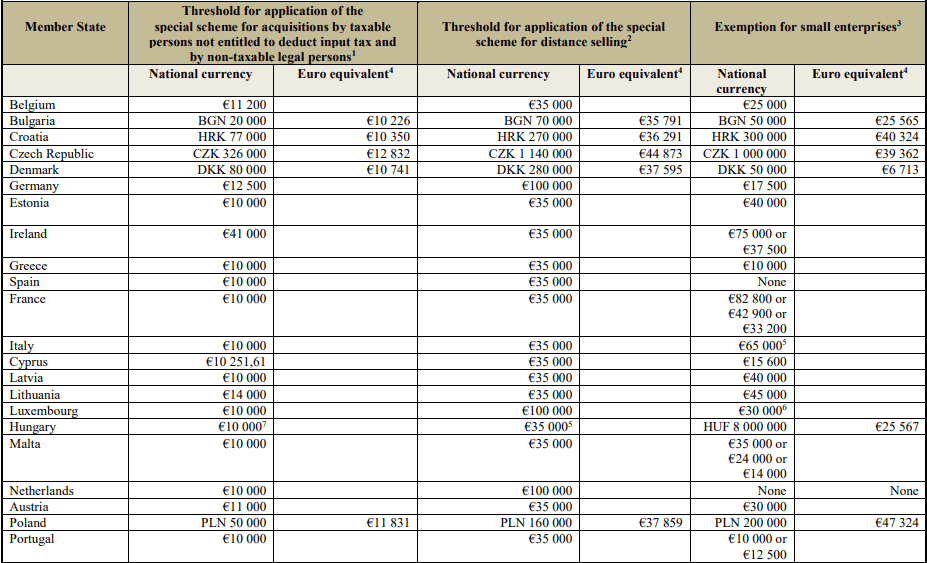

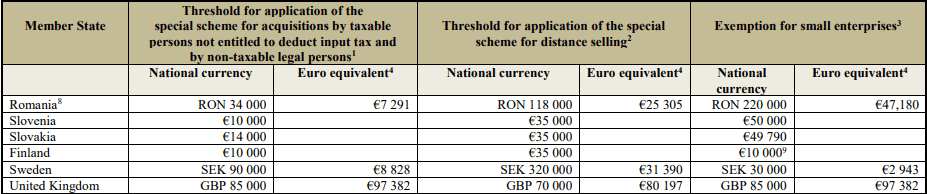

Threshold limits (one more reason why you need to VAT register in Europe):

If you are a company outside of the European Union, and you surpass these limits within the same calendar year, you must VAT register in the country where you exceeded this limit, regardless if you store in this country or not. The threshold limits in Europe are as follows: